April Auto ABS Nowcast: Subprime Breaks Higher

It is tough to make predictions, especially about the future. Auto ABS surveillance gets a little easier when the future has already started filing its remittance reports.

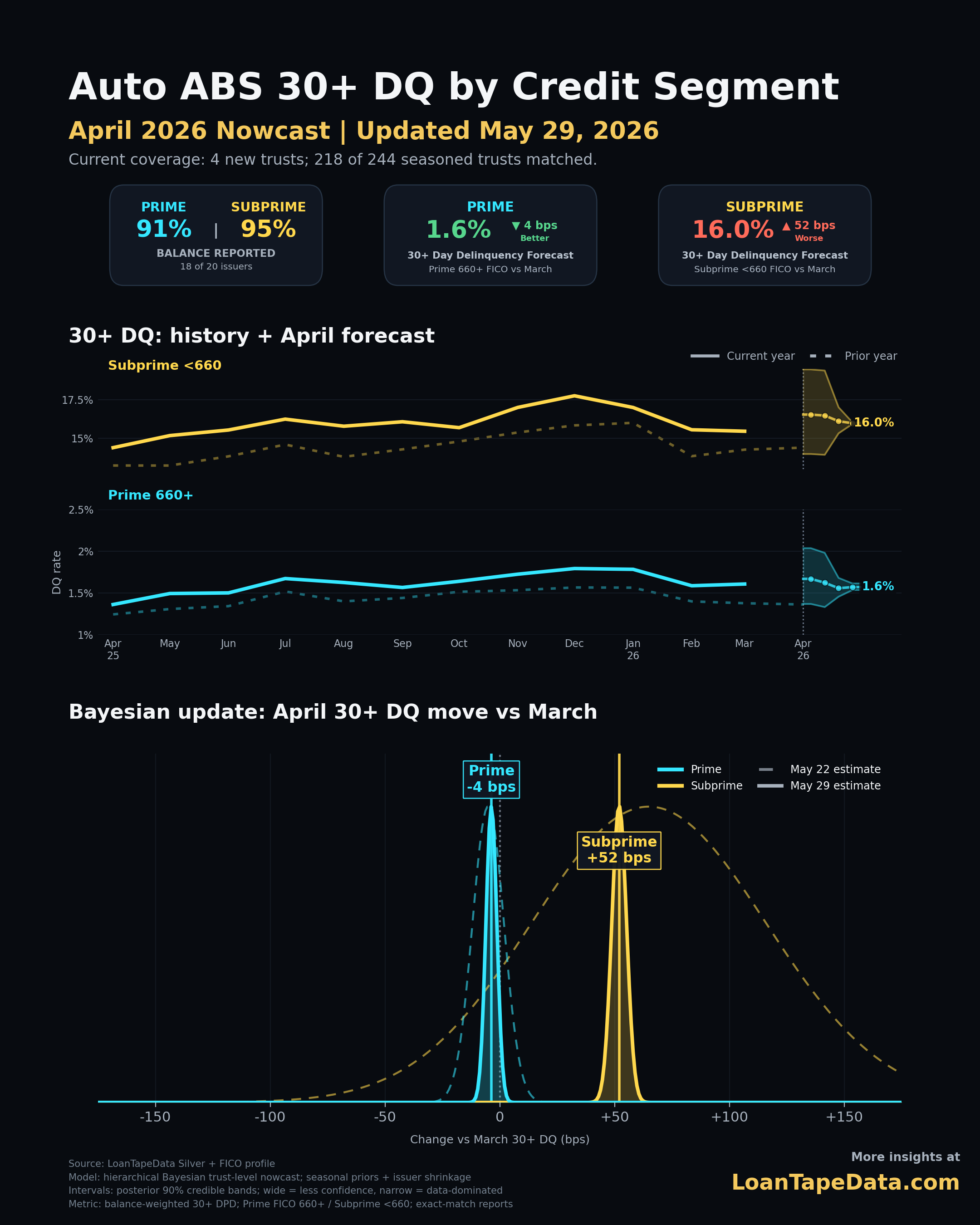

That is where the April nowcast sits. The answer key is not complete, but enough of it is visible. With 91% of prime balance and 95% of subprime balance reported in the May 29 update, the latest LoanTapeData nowcast shows a clean split: prime is holding, while subprime is getting worse.

The all-market April 30+ DQ nowcast is 4.94%, down 66 bps from March. That headline looks fine. The credit-tier read does not. Prime 660+ is nowcasting at 1.57%, down 4 bps from March. Subprime <660 is nowcasting at 15.97%, up 52 bps.

The aggregate hides the split

At the market level, April looks like relief. The 30+ DQ nowcast is below March and below year-ago April. The 60+ DQ nowcast is also slightly lower than both comparison points.

| Metric | March 2026 | April 2025 | April 2026 nowcast | Move vs March | Move vs year ago |

|---|---|---|---|---|---|

| 30+ DQ | 5.60% | 5.18% | 4.94% | -66 bps | -24 bps |

| 60+ DQ | 2.08% | 1.92% | 1.90% | -18 bps | -2 bps |

That table is true. It is also incomplete.

Auto ABS delinquency is a mix of borrower credit, issuer mix, trust seasoning, and reporting order. A cleaner aggregate can sit next to weaker subprime performance if prime is stable and the current reporting mix pulls the total down.

The FICO split is the better read this week:

| Segment | March 2026 30+ DQ | April 2026 nowcast | 90% interval | Move vs March | Balance reported |

|---|---|---|---|---|---|

| Prime 660+ | 1.61% | 1.57% | 1.54%-1.61% | -4 bps | 91% |

| Subprime <660 | 15.45% | 15.97% | 15.93%-16.03% | +52 bps | 95% |

Prime is not the pressure point. Subprime is.

Subprime seasonality just hit hard

Some March-to-April increase is normal. Subprime auto delinquency is seasonal, and one month does not make a full credit cycle.

But size still matters. The April 2026 nowcast is the third-worst March-to-April subprime 30+ DQ move in the LoanTapeData history back to 2017.

| Year | Subprime April 30+ DQ move vs March |

|---|---|

| 2017 | +60.9 bps |

| 2023 | +54.8 bps |

| 2026 nowcast | +52.0 bps |

| 2024 | +34.0 bps |

| 2019 | +28.7 bps |

That is the part I would not bury in the market average. A 52 bp subprime move is not just "seasonality happened." It is a large seasonal hit, and it arrives with most of the subprime balance already reported.

The 90% interval has tightened to 15.93%-16.03%. Earlier in the month, the model had to lean harder on prior history. By May 29, the reported balance is doing most of the work.

Why the nowcast is built this way

Partial filing months are easy to misread.

A new, clean trust can report before older seasoned trusts. One issuer can file a strong deal while weaker seasoned deals are still missing. Reported-only delinquency can look better or worse because the sample changed, not because borrowers changed.

The nowcast handles that by matching at the trust level first. Current-month rows replace only exact issuer, trust, and FICO-segment matches. New trusts are included separately. Missing seasoned trusts stay anchored to their own March delinquency level, then receive a same-calendar-month seasonal roll-forward with issuer and market shrinkage.

In plain English: a new clean trust does not get to stand in for a missing seasoned subprime trust.

That distinction matters most in weeks like this, when the aggregate is calm but subprime is moving.

What to watch next

The next question is whether the subprime 30+ move stays in early delinquency or starts showing up farther down the roll path.

April is mixed. Subprime 30+ DQ is worse than March, but market-level 60+ DQ is still slightly lower. That can happen when early delinquency rises before later buckets catch up. It can also fade if the move is seasonal and borrowers cure before deeper delinquency appears.

The checks from here are straightforward:

- Do the remaining seasoned trusts confirm the subprime 30+ increase?

- Does the 30+ move feed into 60+ DQ in the next one or two reporting months?

- Is the pressure broad across issuers, or concentrated in a few shelves?

- Are newer subprime trusts driving the move, or are seasoned deals weakening?

That last question is why the trust-level method matters. "Subprime is up" is a useful headline. It is not enough for surveillance. We need to know whether the increase came from the same seasoned pools that were already in the March baseline, or from the current-month reporting mix.

Methodology note

This nowcast uses LoanTapeData's recurring Auto ABS DQ nowcast surface. The FICO-segmented visual sources LoanTapeData Silver monthly loan records plus the FICO profile, at issuer + trust name + FICO 660 segment + reporting month grain.

The model forecasts at the trust level first. Existing prior-month trusts are carried forward one by one. Current-month reports replace only exact issuer, trust, and FICO-segment matches. New trusts are added separately. Missing seasoned trusts are forecast from their own March level with same-calendar-month seasonal movement, issuer shrinkage, and market shrinkage. Prime and subprime figures are balance-weighted rollups.

This is a surveillance nowcast, not the final month-end print. It answers the filing-season question: what is April likely saying before every remittance report is in?

The same filing infrastructure powers LoanTapeData's ABS-EE dataset, Form 10-D data, and ABS remittance data. For issuer, trust, and borrower-segment cuts beyond the public chart, see LoanTapeData pricing.