Subprime Auto ABS Affordability Reset

One of the biggest myths in auto finance is that subprime borrower automatically means low income.

It is not a good description of the market today.

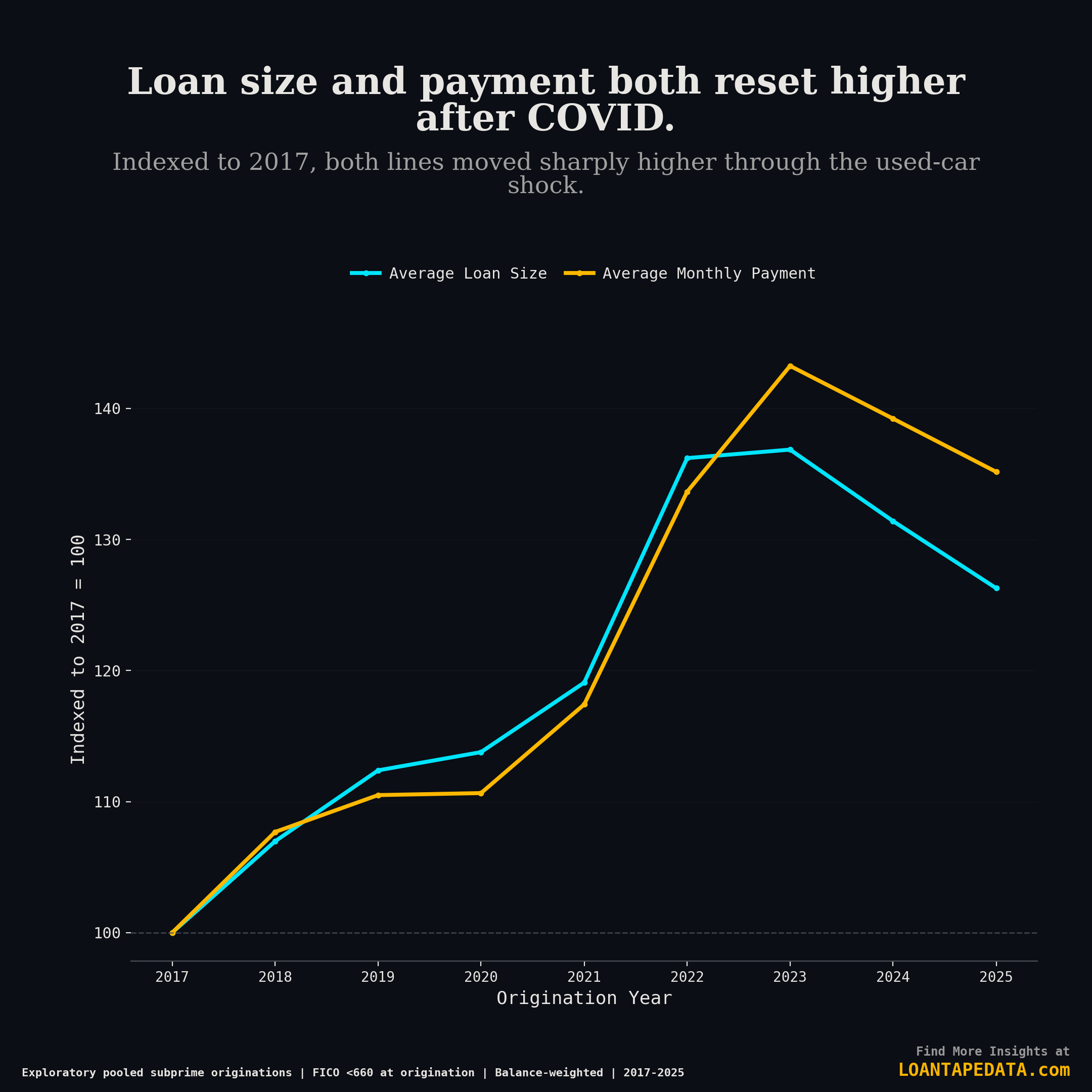

Post-COVID, used-car prices pushed subprime balances and monthly payments sharply higher. In this pooled screen of subprime originations, average loan size went from about $24,000 in early 2017 to a peak near $34,000 during the 2022-2023 shock, and it still sat a little above $31,000 by 2025. Average monthly payment rose from about $510 to about $713 over the same stretch.

If the same borrower base had simply paid more for the same cars, payment-to-income should have blown out. It did not. Weighted average PTI ended 2025 around 11%, only modestly above the pre-COVID range.

So what happened?

The market moved up the income ladder. Higher-income borrowers became a much larger share of subprime, while lower-income borrowers became a much smaller one. At the same time, borrowers shifted into older used vehicles to keep payments workable.

That is the real post-COVID subprime story. The market did not get cheap again. It got more selective.

The payment shock never really went away

The first chart says almost everything you need to know. Loan size and monthly payment both reset higher during the COVID used-car shock. The market cooled from the 2022-2023 peak, but the reset stuck.

By 2025, subprime borrowers were still financing materially larger balances than they were before COVID, and they were still paying materially more each month. That changes the baseline. The old assumption that subprime is mostly a low-income payment story misses what happened next.

Subprime moved up the income ladder

The key question is why PTI stayed relatively contained even as balances and monthly payments jumped.

It was not looser math. It was borrower mix.

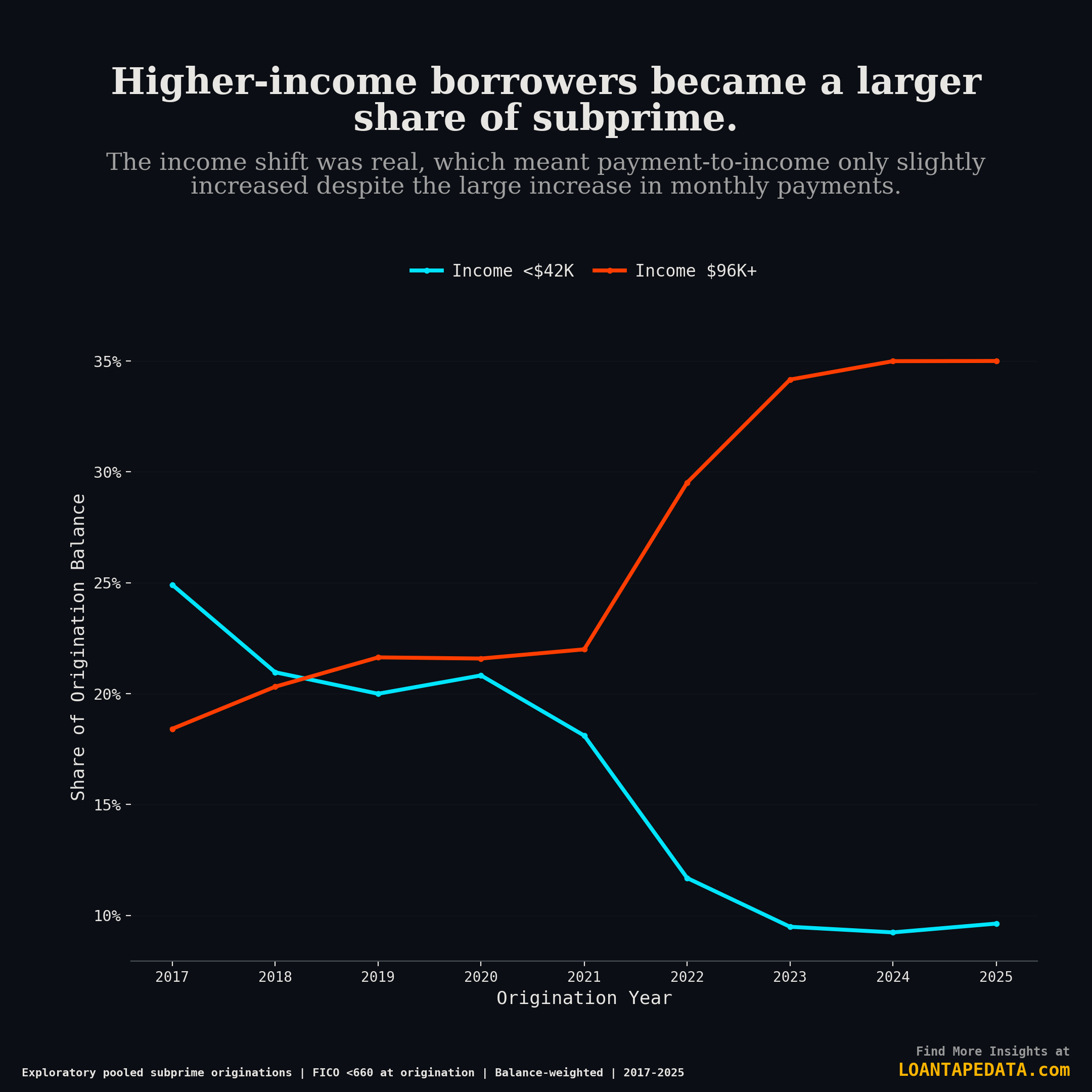

Borrowers with income above roughly $96,000 went from about 18% of subprime origination balance in 2017 to roughly 35% by 2025. Borrowers below roughly $42,000 moved the other way, falling from about 25% of the market to about 10%.

The average income behind subprime originations climbed sharply too, reaching about $88,750 by late 2025.

This is the part many people miss. Subprime did not become a market of lower-income borrowers somehow stretching even further. It increasingly became a market where weaker credit scores sat alongside stronger incomes.

Lower-income borrowers did not disappear from subprime, but they became a much smaller share of it. Higher earners took a larger share because they were better positioned to absorb the higher monthly payment that came with the used-car price shock.

Co-borrowers do not explain the whole move either. Their share stayed within a fairly narrow band over the period. The income lift was broader than that. Lenders screened toward stronger borrowers as payments rose.

Older vehicles helped hold the payment together

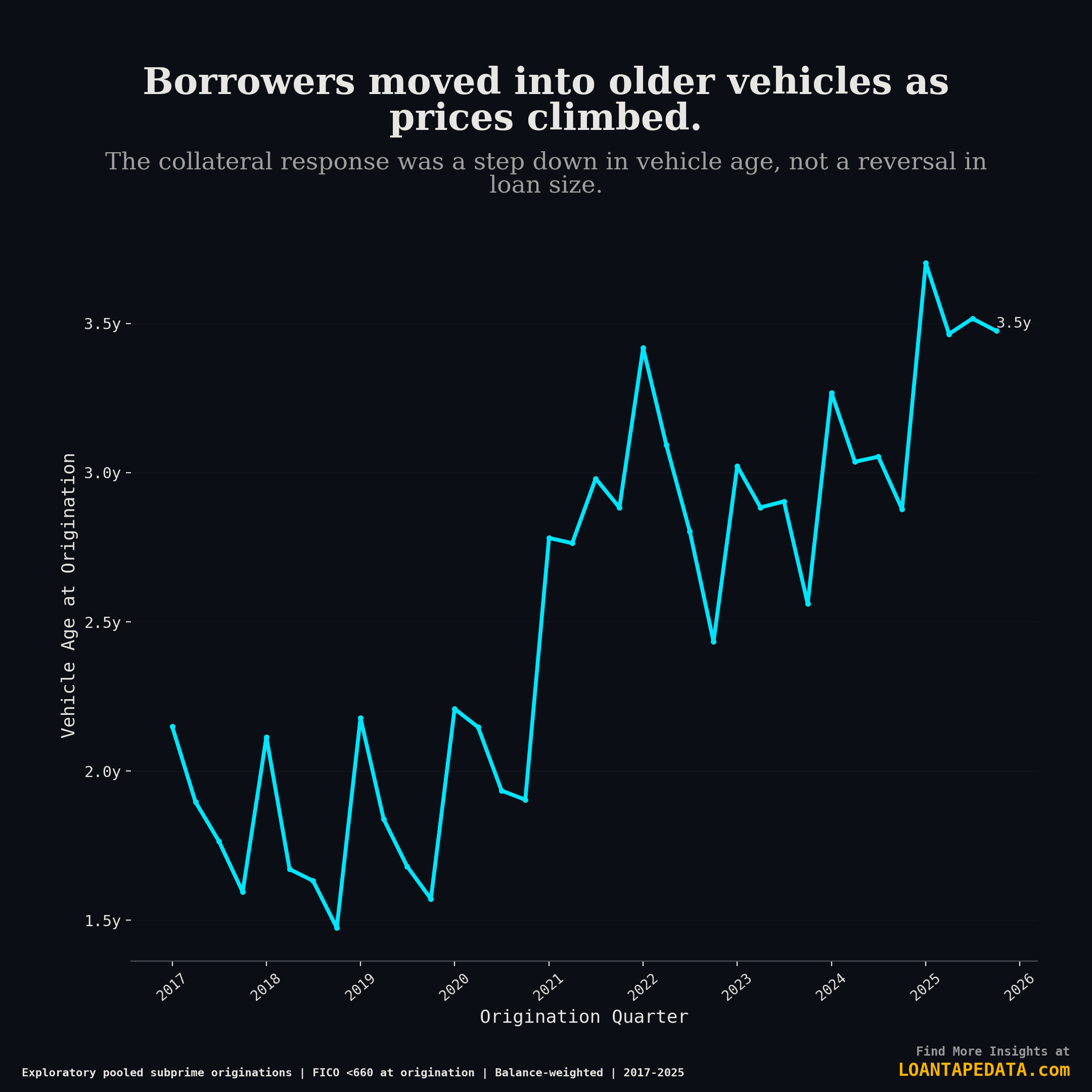

Borrower mix explains part of the reset. The collateral side explains the rest.

Average vehicle age at origination moved from roughly two years in 2017 to around three and a half years by 2025. The used-vehicle share climbed above 80% by late 2025. Borrowers kept deals together by moving into older used cars.

That is not a side detail. It is part of how the market made the payment work. If the car is older, the sticker price is lower than it would be for a newer comparable vehicle, and the monthly payment becomes easier to carry. But that trade comes with its own risk. Older vehicles can mean more repairs, more cash strain on the borrower, and a different loss profile if the collateral starts from a weaker place.

A stable PTI ratio does not capture that tradeoff very well. The affordability reset was absorbed two ways at once: stronger borrower incomes and older collateral. Not a return to the old market.

What this means

Put it together and the post-COVID subprime market looks like this:

- loan sizes reset higher

- monthly payments reset higher

- PTI stayed relatively tight because lender screening got tougher and incomes moved higher

- borrowers also stepped into older used vehicles to keep payments workable

That is why the old stereotype does not hold up very well anymore. Subprime is still about weaker credit quality. It is not automatically a proxy for low income.

A stable ratio can hide a big structural change underneath it. In this case, it hid a market that moved up the income ladder while leaning harder on older used cars.

We update these signals as new ABS-EE filings are parsed into LoanTape's auto ABS coverage. If you want the full chart pack with the bucket-level structure shifts, borrower mix detail, and the rest of the collateral sequence, the full subprime affordability deep dive has the complete deck. The broader loan-level dataset is available through LoanTape's subscription tiers.

Methodology: pooled subprime originations, FICO below 660 at origination, balance-weighted, 2017-2025.