Auto ABS Trust Adds: March 2026

Most pool surveillance starts with delinquency. That makes sense, but it is late. By the time delinquency moves, the mix shift is already in the book.

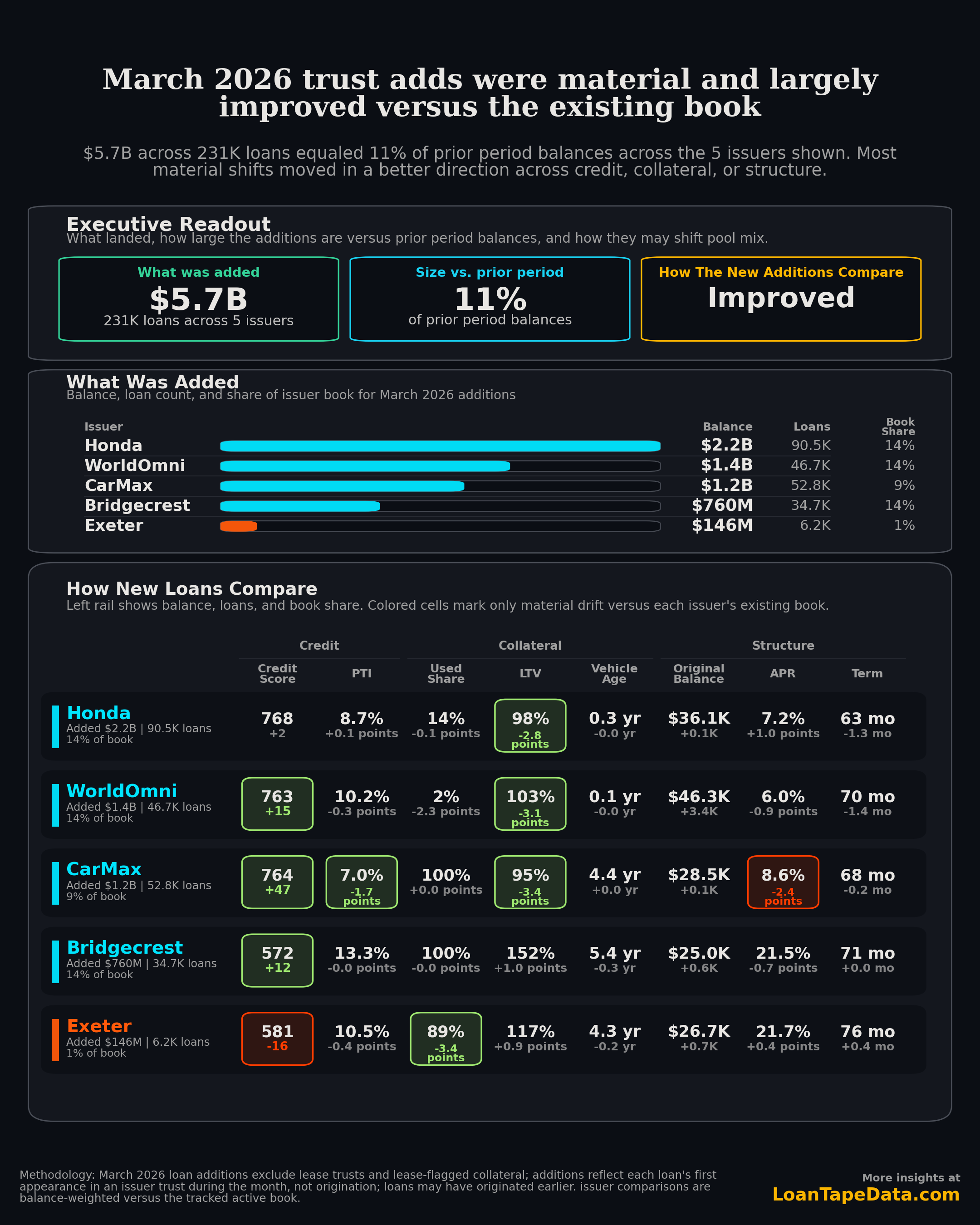

March 2026 first-seen loan trust additions totaled $5.7 billion across 231,000 loans for the issuers captured in this screen. That was equal to 11% of prior-period balances across Honda, WorldOmni, CarMax, Bridgecrest, and Exeter.

The headline is constructive. Most of the material shifts moved in a better direction versus each issuer's existing active book, especially across borrower score, LTV, PTI, used share, or APR. The March add was not uniform issuer by issuer, but the overall read was more improvement than deterioration.

For this screen, "first-seen trust additions" means the first month a loan appears in an issuer trust. It does not mean the loan originated in March. It means March 2026 was the first month it showed up in the trust data. Lease trusts and lease-flagged collateral are excluded from this loan-addition view because their lease fields do not map cleanly to the loan metrics in the matrix.

What March adds looked like

| Issuer | Added balance | Added loans | Share of issuer book | Main takeaway |

|---|---|---|---|---|

| Honda | $2.2B | 90.5K | 14% | Largest March loan add by balance; mostly near book, with LTV lower at 98% versus 101% and APR higher at 7.2% versus 6.1%. |

| WorldOmni | $1.4B | 46.7K | 14% | Cleaner mix: FICO rose to 763 from 748, LTV fell to 103% from 106%, and APR fell to 6.0% from 6.9%. |

| CarMax | $1.2B | 52.8K | 9% | Broad improvement: FICO rose to 764 from 717, PTI fell to 7.0% from 8.7%, LTV fell to 95% from 98%, and APR fell to 8.6% from 11.1%. |

| Bridgecrest | $760M | 34.7K | 14% | FICO improved to 572 from 560 while most other risk fields stayed close to book. |

| Exeter | $146M | 6.2K | 1% | Small add with mixed characteristics; the size is too small to drive the overall March read. |

Honda is the largest March loan addition. That matters even when the mix is close to book. A $2.2 billion addition can still move pool composition if the flow persists, and the main difference in this cut is not borrower score. It is collateral and pricing: LTV is lower, while APR is higher.

Additions Mostly Improved

CarMax is the cleanest signal in the March add set. The added loans were still essentially all used vehicles, but borrower and pricing metrics moved in a better direction. FICO rose 47 points to 764, PTI fell by 1.7 points, LTV fell by 3.4 points, and APR fell by 2.4 points versus the existing active book.

WorldOmni also screened better across the major risk fields. The add was $1.4 billion, FICO rose 15 points, LTV fell by 3.1 points, and APR moved lower. Bridgecrest showed a smaller but still positive credit-score move, with FICO up 12 points while most other fields stayed close to book.

The important point is not that every issuer moved cleaner on every metric. They did not. The point is that the material March changes were mostly improvements, and the biggest additions by balance did not show a broad deterioration in risk mix.

What To Watch Next

- Persistence. A cleaner add matters more if it repeats in April and May.

- Book-share effects. Honda, WorldOmni, and Bridgecrest each sit near 14% of issuer book in this pull, enough to matter even when drift is not dramatic.

- Lease trust treatment. Lease trusts and lease-flagged collateral should stay out of this loan-addition matrix unless they are handled in a separate lease view.

- Smaller adds. Small issuers or small monthly adds can show sharp metric moves without changing the overall issuer book.

We update this screen as new ABS-EE filings are parsed into LoanTape's auto ABS coverage. The broader loan-level dataset is available through LoanTape's subscription tiers.

Methodology: first-seen loan trust additions by issuer for March 2026, excluding lease trusts and lease-flagged collateral; balance-weighted comparisons versus the existing March 2026 active book; field-level metrics computed on the covered-balance subset for each metric.