Auto ABS Trust Adds: February 2026

Most pool surveillance starts with delinquency. That makes sense, but it is late. By the time delinquency moves, the mix shift is already in the book.

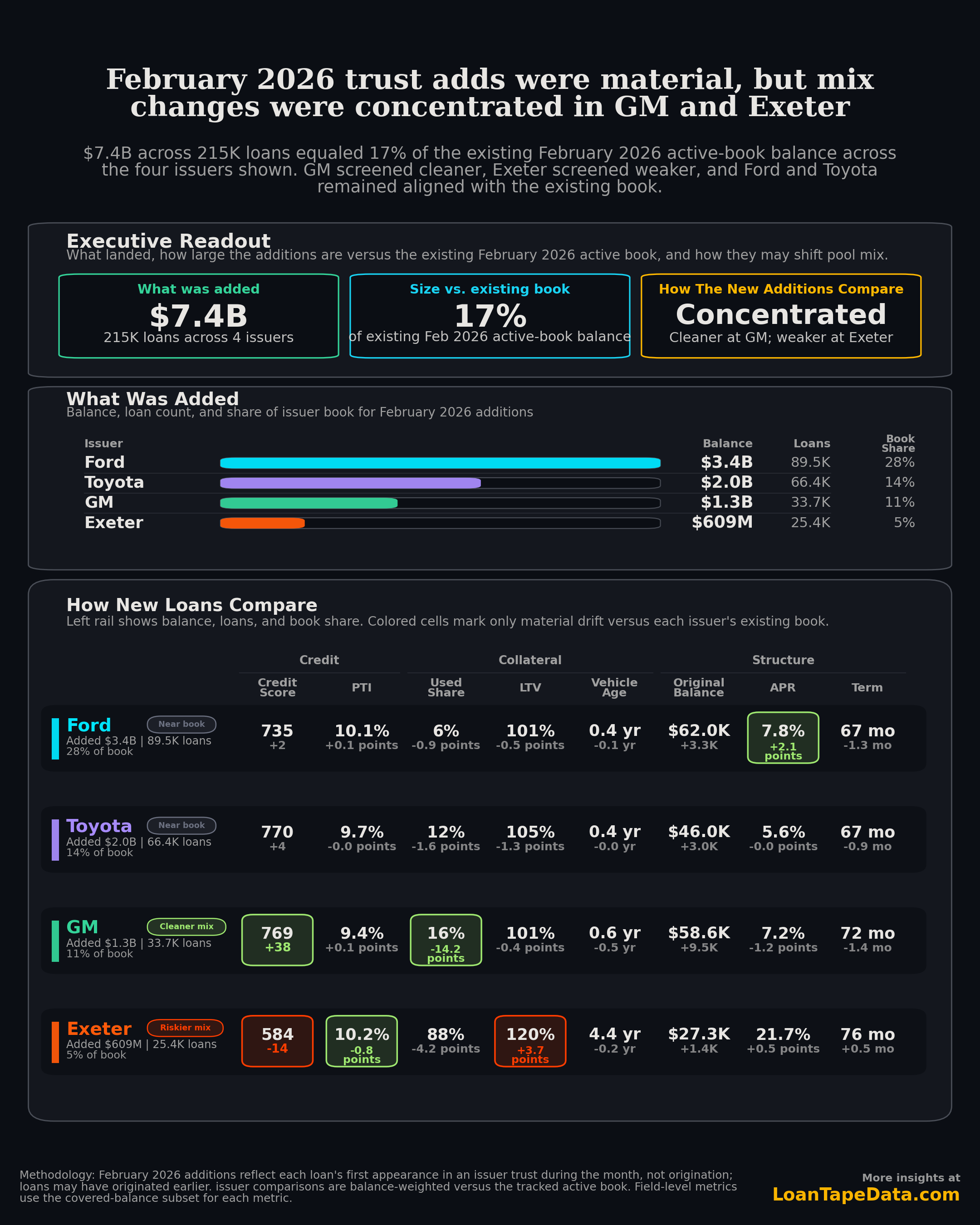

February 2026 first-seen trust additions across Ford, Toyota, GM, and Exeter totaled $7.4 billion across 215,000 loans. That was 17% of the existing February 2026 active-book balance across the four issuers shown. GM's additions came in cleaner than its existing book. Exeter's came in weaker. Ford and Toyota were mostly in line with the books they were joining.

For this screen, "first-seen trust additions" means the first month a loan appears in an issuer trust. It does not mean the loan originated in February. It means February 2026 was the first month it showed up in the trust data.

What February adds looked like

| Issuer | Added balance | Added loans | Share of existing book | Main takeaway |

|---|---|---|---|---|

| Ford | $3.4B | 89.5K | 28% | Credit and structure stayed close to book, but APR rose to 7.8% from 5.7%. |

| Toyota | $2.0B | 66.4K | 14% | Broadly aligned with the existing book, with a modestly higher FICO and slightly lower used share. |

| GM | $1.3B | 33.7K | 11% | Cleaner adds: FICO rose to 769 from 732, used share fell to 16% from 30%, and APR fell to 7.2% from 8.4%. |

| Exeter | $609M | 25.4K | 5% | PTI improved to 10.2% from 11.0%, but FICO fell to 584 from 598 and LTV rose to 120% from 116%. |

Ford added the most balance by a wide margin. That matters by itself. A near-book addition can still change the pool if it comes in size. Here the mix stayed close on FICO, PTI, LTV, vehicle age, and term. The obvious change was pricing. New adds came in at 7.8% APR versus 5.7% on the existing book.

Toyota looked similar. The additions were meaningful, but the mix shift was modest.

GM improved, Exeter weakened

GM was the standout in a good way. The new loans had materially higher credit scores, much less used-vehicle exposure, a lower APR, and a slightly shorter term than the existing active book. FICO rose to 769 from 732. Used share fell to 16% from 30%. APR fell to 7.2% from 8.4%. If that pattern holds, GM's performance stats should get some help from mix before they get help from seasoning.

Exeter was the opposite case. PTI improved to 10.2% from 11.0%, but FICO fell to 584 from 598 and LTV rose to 120% from 116%. That is the sort of split signal that can fool you if you only watch one ratio. The affordability number looks better. The borrower and collateral mix does not.

That is why this cut is useful. The headline volume matters, but the internal mix matters more. Two issuers can add meaningful balances in the same month and still be moving in opposite directions on pool quality.

What to watch next

- Ford pricing. If APR stays elevated while the rest of the risk stack stays flat, pricing may be moving before the usual credit metrics do.

- GM mix quality. Cleaner adds only matter if they keep showing up as volume grows. Watch whether the higher FICO and lower used share stick.

- Exeter's split signals. Better PTI does not cancel out weaker FICO and higher LTV. If this mix persists, watch both delinquency roll rates and severity.

- Volume versus book size. Even near-book additions matter when they come in this size. Ford's 28% and Toyota's 14% shares are not rounding errors.

We update this screen as new ABS-EE filings are parsed into LoanTape's auto ABS coverage. The broader loan-level dataset is available through LoanTape's subscription tiers.

Methodology: first-seen trust additions by issuer for February 2026, balance-weighted comparisons versus the existing February 2026 active book, field-level metrics computed on the covered-balance subset for each metric.